We have just completed the process of buying a house and have spent quite some time looking in to various aspects of property buying and owning in Denmark. This is a compilation of the things we have learned.

Most of the links in this article will unfortunately be to pages in Danish. I have not been able to find that much information in English.

Where to look?

There are two good websites that collect more or less all houses for sale in Denmark. They both offer you the possibility to create a user profile and get alerts when houses matching your criteria come for sale. Neither has an English interface.

Boliga.dk is an independent site that collects data from the differentreal estate agents. Some of the good features about Boliga are:

- Get email alerts to let you know when new houses are for sale in your area.

- Get email alerts when houses on your watch list have an open house.

- You can see what a house has been sold for previously and what the reduction in asking price is.

- Houses sold by owner are only listed on Boliga not Boligsiden. Same goes for (very) few real estate agents.

Boligsiden.dk is owned by an association of real estate chains. Some of the good features of boligsiden are:

- They get new listings a day before Boliga

- You can limit your searches to an area you mark on the map

- If you add a house to your “Huskeliste” (favorites) you can see how many other people have “fav’ed” it and how many people look at it.

Some of the interesting facts you can see on the sites are:

How to compare?

The mantra for real estate agent are location, location, location. But there is a couple of other things you can look at in your hunt.

Ask thereal estate agent of a house for the reports and they will send you at least four documents:

- Sales Report (Salgesopstilling)

- Building Survey (Tilstandsrapport)

- Electricity Survey (Eleftersyn)

- Energy Report (Energirapport)

These all follow the same standard for all houses so there will be a multitude of parameters which you can use in comparing two or more interesting houses. Here are some of the ones I would like to highlight.

Price per square meter

From the Sales Report you can see the price per m2. It is public data what the m2-price is in any area split by postcode. So by looking at the m2-price of a house you can get an idea of whether it is above or below the average for an area.

Condition of the property

The building survey will give an overview of the house comparable to its age. A surveyor will go through the house and check for visible faults and errors. The damages are rated according to this scale:

- K0 = Cosmetic

- K1 = Less serious damage

- K2 = Serious damage

- K3 = Critical damage

This does not tell you how expensive it will be to fix the error but how critical it is to maintain the property’s integrity. For instance, often bathrooms will have lose tiles (K1s or K2s) and outside wood on the house needs painting (K2s or K3s).

The electrical survey is done in a similar way.

Energy rating and costs

Denmark is a cold country and energy costs are a big part of having a house. All houses for sale have to have an energy rating done and you can use this to get an idea of what heating the house will cost you.

The scale goes from A2020 where a 140m2 house costs 1800-3500dkk per year to heat up to G where a 140m2 house cost 26000-35000DKK per year. Compound that to 10-20 years of ownership and you can see that energy costs is a factor to consider.

Roughly speaking moving one step to the left of the scale is equal to a price increase of 800dkk per m2 according to research. If you make certain energy saving initiatives you can improve your energy rating and thereby lower your costs and improve the (potential) value of your house.

In the Sales Report you can see the current owners’ yearly cost of heating. This can vary greatly from the Energy Rating of the house as they might not heat parts of a house or have it colder or warmer than the norm.

Find background information

More and more data in Denmark is getting digitized and the public sector is making good efforts to make it accessible for free. This is to your advantage as you can find a lot of things for free and some sites make it very easy to check things.

Dingeo is a fairly new but really interesting site. If you have an address it lets you find useful information about things like:

- Radon level – This is on kommune level, so don’t panic. For Sønderobrg area the kommune is in a risk zone of Radon, so don’t sleep in the basement if you smoke – or measure the Radon if you do.

- Ground pollution (Jordforurening) – What polluting businesses have been on the plot or vicinity in the past. The house might sit on top of an old landfill (as is the case with Møllegade in Sønderborg).

- Risk of flooding (Oversvømmelsesrisiko) – Climate change has meant warmer and wetter climate in Denmark and that is probably only going to get worse. Avoid buying a house built in a place that used to be a bog or a meadow.

- Traffic noise (Trafikstøj) – At the moment this feature can only be used in bigger cities but as the data gets better this may have an impact on house prices as air and noise pollution get more focus.

- School rating (Skoler) – Grade averages (Karakter gns), parents net income (Bruttoindkomst) and absent rate (Gns. Fravær) might be used to give you an indication of the people in the neighborhood.

Tinglysning is the public record of who is the legal owner of a property. (Enter street, house number and post code to search). You can also see which mortgages or pledges there are on the property. So you can see how much the current owner put in a mortgage at the time they bought the house. You can compare that to the “Salgsopstilling” where it often says how much they still owe on a house.

Mortgage and costs

Today there are a multitude of ways to borrow money for a house in Denmark. So here is the simplified version.

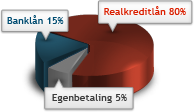

80% of a loan can be made as a mortgage (Realkreditlån). The rest of the borrowed amount you either have to pay as a down payment or get a bank loan (banklån). Depending on your relation with your bank they will require you to make a down payment of somewhere around 5% of the borrowed amount.

The two main variety of loans are Fixed Rate Loans (Fastforrentet lån) or Adjustable Rate Mortgage (Rentetilpasset lån). What to choose depends on your risk profile, life choices and finances, so you need to talk to a professional for advice. To see what you could end up paying for different loan amounts try this Loan Calculator.

The traditional mortgage model in Denmark (PDF link) is well regulated by law so you are fairly protected as long as you pay your dues. There are four mortgage institutions in Denmark: Realkredit Danmark, Nykredit, BRFKredit, Nordea. All of them are now owned by banks and the prices are pretty much the same – here’s a price guide. You can’t bargain about the interest rate but if you let your other bank business follow your mortgage you can negotiate about fees.

For the bank loan bit it is all up to the bank to decide, so here the different banks will offer you different products and prices depending on how they evaluate your finances.

You get a tax discount of about 33% of the interest you pay on a mortgage per year. So if you borrow 2 million fixed at 2,5% for 30 years your monthly payment is 9500dkk before tax and 7680 dkk after tax.

The “bidding game”

It is quite common that there is a negotiation going on about the price of a house and unless you are buying in a red-hot market it is of great financial benefit for you to know what the market price is and how much to bargain for. The longer the house has been on the market the more likely it is that you can squeeze the price.

The good thing with the publicly available data on, for instance, Boliga is that you can see how other people have bargained. In Sonderborg at the moment houses sell for 6-10% lower than the asking price. (And the asking price might have already been reduced if the house didn’t sell quick) See Actual house sales and how much they were reduced in price.

Get professional help

Remember that the real estate agent is the “seller’s guy”. He is typically paid a percentage of the sale, so his interest is in creating a quick sale for the highest possible price.

The bank “advisor” is also not there for you but to make money on you and he can be paid a commission based on what loan you chose.

So do yourself a favour and either do a lot of research into the field or spend money on professional help. You only have to get professional help to sign the deed but the money is most likely well spent.

The advisors I would suggest you consider consulting are:

– A builder/carpenter or construction technical advisor (Byggeteknisk rådgiver) can help you asses the general condition of the house and which repairs you need to plan and what they might cost. The Building Survey covers some of these areas but it does not give you a complete picture of the house. If you have a local network you can also ask around for a reputable carpenter to see if they want to consult for you.

– A lawyer to write the deed but also to guide you through the legal implications of a house sale.

– An independent financial advisor who can help with financial overview and explain the different loan types, help you choose the right loan and negotiate with the bank.

Buying a house as a non-Dane

If you are not a Danish citizen there are special rules for buying a house.

In order to buy property in Denmark you need to be residing in Denmark (be in the country for at least 180 days a year). If you as a EU citizen live and work here this is just a checkbox on a form. If you are not from EU or you do not live here permanently you need a special permit from the Ministry of Justice.

If you do not comply with the rules you can be forced to sell your property. So if in doubt talk to a lawyer.

Costs of buying a house

These are some ball park figures of what the one time costs are to buy a house in Denmark:

- Deposit: Minimum 5%-10% of the sales price

- Notary of loans (Tinglysning) from 8,000dkk – 37,400dkk depending on current loans in house and cost of house.

- Standard lawyer fee for writing the deed from 4,000 – 10,000dkk

- Owner change insurance – 10,000 – 20,000dkk (optional but advisable)

The running costs depend on the house but they include:

- House insurance

- Utilities (Water, electricity, power)

- Garbage removal

- TV license

- Property tax

- Property value tax (for the kommune)

An example of different types of family budgets can be found here.

Updated 11/2/2017: Link to budget changed as old link was dead.